The disappointing US labor report last Friday left a lot to ponder over the weekend. With the majority of market players on holiday, how and when will the market digest this data point?

Charts Courtesy of Yahoo Finance.

With only an abbreviated futures trading session, and bond markets closed on Friday, the markets had little opportunity to react to a sub-par US employment report. This makes for heightened anticipation to see markets in motion this week. With most of Europe closed on Monday and US players partly on school holiday, it may take some time for this scenario to play out. An academic, though market related, argument for US interest rate hikes gets a bit more complicated. While there has been signs that the US economy has slowed ever so slightly, it is hard to say whether the causes were short term or more due to the structure of the US economic recovery.

There have been two main stalwarts in the markets this year: the strength of the US dollar and the decline of oil prices. Those two dynamics have been forces of nature this year. They come with consequences and many lasting effects on economies and at some point eventually markets. If the US economy has been the shining star of the past few months, the strength of the dollar has certainly been a corroborating witness.

This dollar strength has also meant that US goods that are exported will have less of a global demand. It also means that foreign goods imported into the US come at a discount to US consumers. This logically will result in a squeeze of US manufacturers. Even though manufacturing does not have the same weight as it once did in years past, it is still relatively important in that a lot of capital has recently been spent looking to jump start manufacturing in the US.

Along the same train of thought, the oversupply of oil has come with its own consequences. Shifts to cleaner and more sustainable technologies has put a damper in the demand of oil. While this has not been a main catalyst, it is a constant reminder that alternative energy sources have been and will continue to be developed. The US has also invested a lot of capital at becoming oil independent. However, most of the investment in the technologies and production of oil has been made with an oil price forecast that was higher than the current markets. The profitability, not to mention the viability, of many of these investments comes into question with lower oil prices this soon in the business cycle. Could some of the jobs produced from the oil investment go away soon? What long term effects could this have on the economy or more importantly, what does this do to equity markets? It is asking these essential questions that help form a context for coming up with trade ideas.

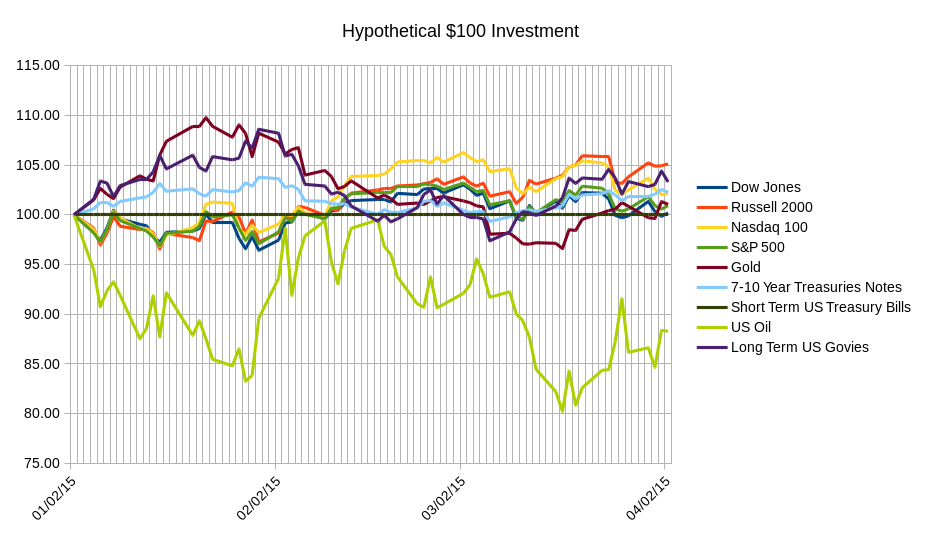

Changing the focus to broader investments, a hypothetical investment in the beginning of the year illustrates the tightly bound nature of most asset classes with the exception of oil. After an initial divergence of total return, most asset classes converged around the middle of February and became slightly more correlated. This condition of these various assets being more correlated has been the norm since around 2012.

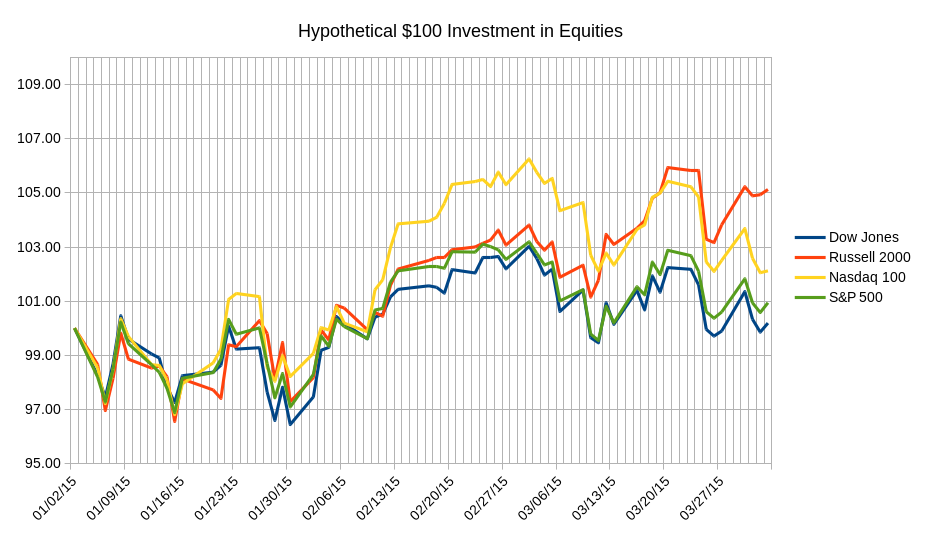

Looking more deeply into the equity market performance we see that riskier stock indices like the smaller cap Russell and the tech-heavy Nasdaq indices have led the way this year so far.

Looking more deeply into the equity market performance we see that riskier stock indices like the smaller cap Russell and the tech-heavy Nasdaq indices have led the way this year so far.

This year the convergence of equity markets has typically come with dips in the equity market. This is in contrast to having more traditional indices and blue chip names catch up.

This year the convergence of equity markets has typically come with dips in the equity market. This is in contrast to having more traditional indices and blue chip names catch up.

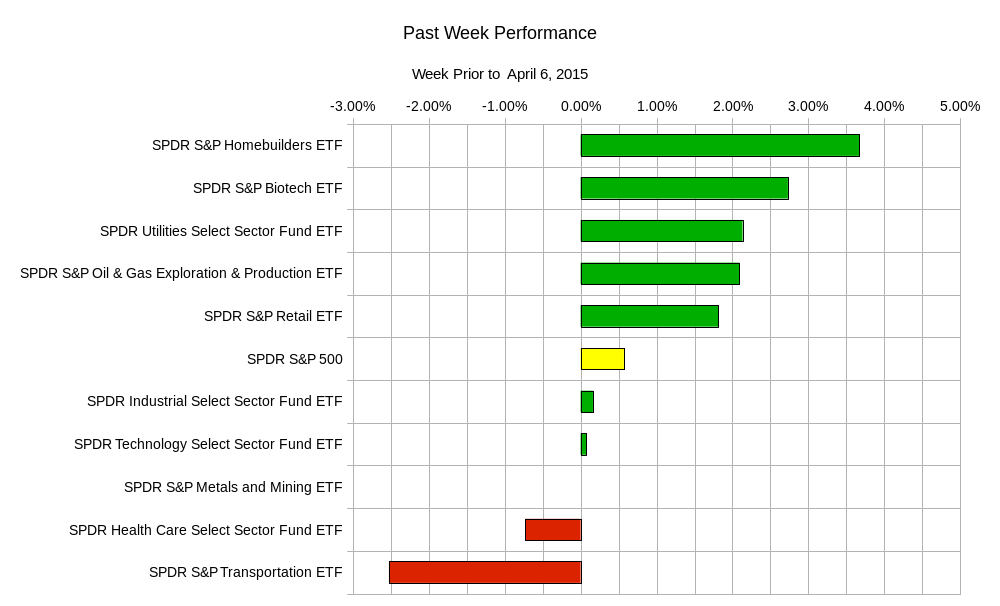

Looking at this past week we see the components of the S&P 500. Interestingly enough is the under-performance of transports. Could this be signalling a temporary spike in oil prices, or a pause in the decline?

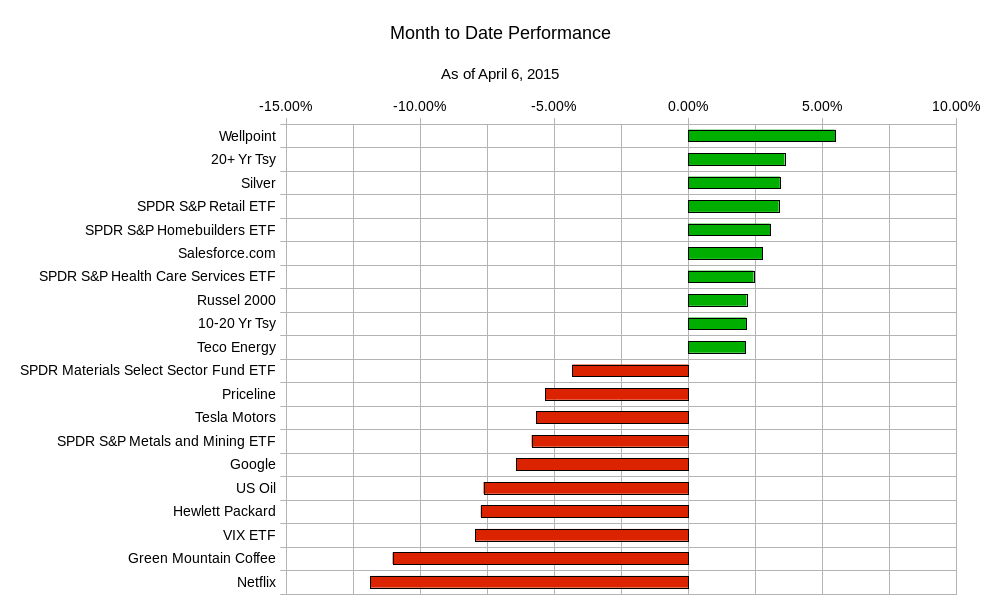

Taking a step back and looking at how broader markets have evolved over the past month we see the following results:

Taking a step back and looking at how broader markets have evolved over the past month we see the following results:

Of note is the performance of US Government bonds in the face of interest rate hikes. Perhaps the market sees very cautious and conservative FOMC rate hike action. This makes this Wednesday’s meeting minutes release an interesting one to watch. Could the language of the Federal Reserve Board contrast with the recent employment data? Was this recent job report an aberration or a sign of things to come?

Of note is the performance of US Government bonds in the face of interest rate hikes. Perhaps the market sees very cautious and conservative FOMC rate hike action. This makes this Wednesday’s meeting minutes release an interesting one to watch. Could the language of the Federal Reserve Board contrast with the recent employment data? Was this recent job report an aberration or a sign of things to come?

On the topic of data releases, here is the calendar for this week:

Monday – Japan – Leading Economic Index, US Non-Manufacturing PMI, US Composite PMI, Canada PMI; Tuesday – Royal Bank of Australia Interest Rate Policy Statement, Spain Services PMI, Euro-zone Services PMI, US Consumer Credit; Wednesday – Bank of Japan Monetary Policy Statement, US Federal Reserve Board Meeting Minutes; Thursday – German Industrial Production, Bank of England Interest Rate Policy and Asset Purchase Decisions; Friday – Canadian Unemployment Report

For the week, the most popular ETF ranges are likely:

| ETF Ranges for Week Ending April 10, 2015 | |||

| Ticker | Ticker Name | Lower Range | Upper Range |

| SPY | S&P 500 ETF | $202.40 | $210.00 |

| QQQ | NASDAQ-100 ETF | $103.20 | $107.70 |

| IWM | Russel 2000 ETF | $121.60 | $127.70 |

| TLT | 20+ Year US Treasury ETF | $128.60 | $133.80 |

| USO | US Oil ETF | $16.90 | $18.00 |

| GLD | Gold ETF | $112.20 | $118.00 |

Asking essential questions about economic factors and causes and effects on markets is an important part of a trading thesis. In collaboration with other techniques like chart analysis and other quantitative studies, ideas from macroeconomic factors help generate trading and hedging strategies. It also keeps existing trades in check by forcing you to constantly question your investments.

Good luck and trade rationally.