if you felt like the market was stuck in mud then you should be happy with the volatility we have now. Be careful what you ask for, you might just get it.

Last week started off with some selling on Monday that was met with cautious optimism the next two days. The US Federal Open Market Committee released their meeting minutes on Wednesday and bullish sentiment prevailed. The market immediately reacted to the minutes with strong buying. The minutes led investors to believe that the Fed is more “dovish” than what was believed. The term dovish refers to policy that leans towards keeping interest rates low in an effort to stimulate an economy. This is opposed to “hawkish” policy, that in contrast, is meant to keep inflation in check by keeping interest rates high, therefore keeping an economy from reaching unsustainable growth. The Fed attempted to reverse previous hints that interest rate hikes were coming sooner rather than later. This led the market to believe that the fear of higher interest rates was a bit excessive, at least for the time being. Then the hammer fell on Thursday, with traders swiftly taking profits from the Wednesday afternoon rally. The selling continued despite any sort of new information. Friday saw the release of disappointing earnings news from JP Morgan Chase, and the selling continued. Typical of 2014 so far, Friday was a day to sell and not go long into the weekend.

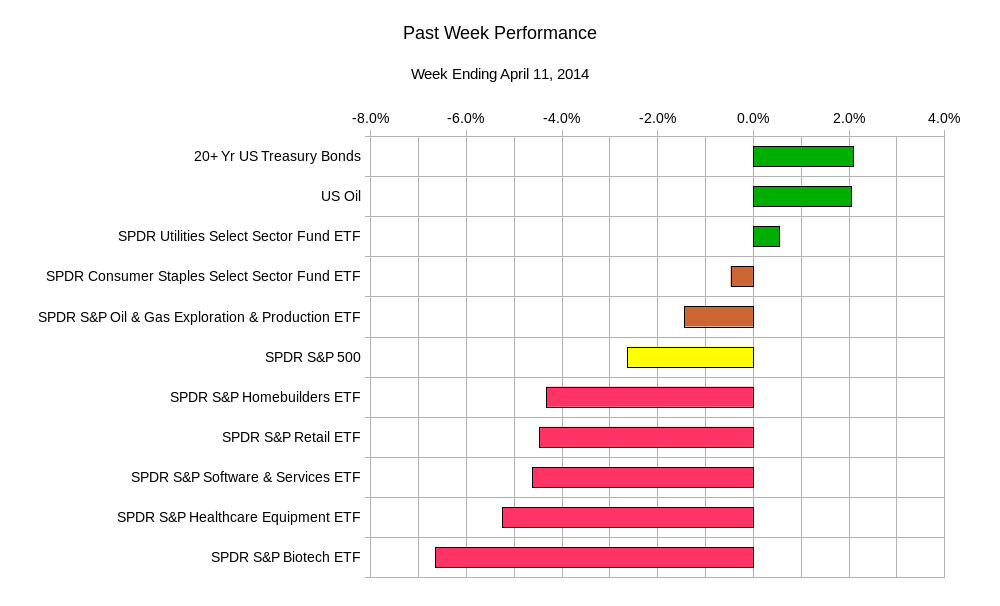

It seems that this recent market drop, currently at about 4.5% from the recent highs in the beginning of the month, is a reflection of traders questioning the valuation of stocks. Up until this past week, the selling has been in more volatile equity names and sectors. The selling was limited to investments that appear to be riskier and do not have the steady flow of revenues and profits that conservative names tend to have. This was apparent by looking at how consumer staples and utilities sectors gained while traditionally speculative sectors like biotech and technology were sold. This past week the selling was broad based and no sector was safe. The only winners were US WTI Oil and longer maturity US Government bonds. As you can see even the traditionally conservative sectors could barely catch any buyers.

This could be the beginning of the signs of further selling pressure. Certainly by now this market has begun to think aloud about whether or not recent prices represented true value. The earnings season will help clarify traders thoughts. Though it may not end well for some stocks. JP Morgan Chase suffered a 3.3% drop upon release of its earnings report. It is truly a buyers beware type of market in the near term. It is not to say that rallies are not possible, but they are more than likely to be short lived until investors feel comfortable with the price they are paying for equity securities.

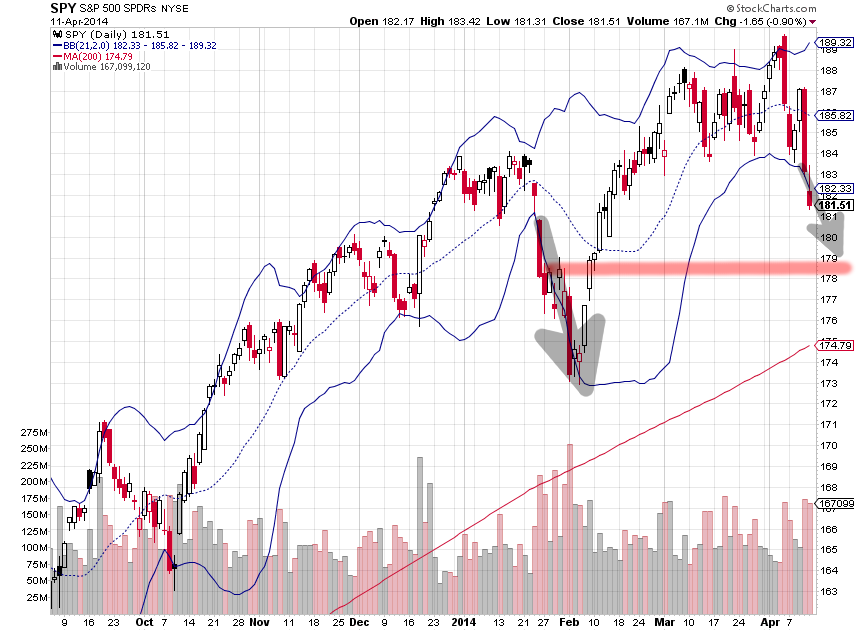

One ominous sign is seen in the chart for the SPY, S&P 500 ETF. You can see that when the chart is overlaid with Bollinger Bands. Bollinger bands are lines that are drawn at +2 or -2 standard deviations of stock price changes from the current average price. In practice, these bands represent the range of the stock price changes about 97.7% of the time. When a stock is trading at or through one of these bands it is sometimes considered to likely revert to an area in between the bands. It seems intuitive at first. The price should not spend too much time outside of the band. The band should only be broken less than 3.3% of the time. However, do not get tricked by the Monte Carlo Fallacy. The band is a moving target so that it is dynamic and could get wider which could keep the price in between the bands, albeit at a much lower or higher price. As we can see here, the lower Bollinger band for the SPY ETF is a slippery slope. The last time it was tested at the end of January, it fell down that slope resulting in a further decline of about 3.7%. At this moment, we seem to be at the beginning of another slope. Perhaps the SPY can slide some more. If it did, it appears that the area of $178.50 could provide some support. Interestingly enough, the fall from new highs in late January ended at about 6% lower than those highs. Currently the $178.50 level represents a 6.3% discount to the all time highs. After the selling in late January to early February subsided, the SPY rallied almost 9.5%.

Chart Courtesy of StockCharts.com

Chart Courtesy of StockCharts.com

It would appear that the easier trade is to the short side until we see hesitation in the selling. Again, this may only be a bump in the road. It seems bearish sentiments are beginning to prevail. Once it is overdone, or rather once the patient and opportunistic investors feel like they have a large enough discount, things can reverse quickly. Just as they did in February. In the way it was easy to be long for most of the year, it will be easy to be short in the near term.

This week may see the SPY ending somewhere in between $178.50 and $186.00.

This will be a busy week. It is a short week as equity markets are closed on Friday in observance of Good Friday. Also many participants may be on holiday for Passover. Most primary education schools in the US will also be on holiday, meaning the trader parents are likely to also be on holiday. Increasing tensions between Ukraine and Russia also add to the market dynamics. Earnings will also play a role, as a diverse set of companies report this week. This week also has a busy economic data calendar. Monday will have US Retail Sales; UK Consumer Price Index and US Consumer Price Index on Tuesday; China GDP, Euro Consumer Price Index, US Housing Starts, and US Industrial Production on Wednesday; US Jobless claims, and US Philadelphia Manufacturing Survey on Thursday.

On the earnings front: Citigroup reports on Monday; Coca-Cola, Intel, and Johnson & Johnson on Tuesday; American Express, Bank of America, Google, and IBM on Wednesday; General Electric, Goldman Sachs, Honeywell, Morgan Stanley, Pepsico, Schlumberger, and United Health Group on Thursday.

For a shortened week there is no shortage of market information to be digested. This may prove to be one of the more volatile weeks as of late. Recognize, that when news is released it is less about the news and more about the liquidity that will be presented to you. Especially during holiday weeks, it is important to be prepared for when the liquidity dries up and the market seems to be locked in. Stay nimble and be prepared with a game plan.

Good luck and trade rationally.